FUNDING AND TREASURY

FUNDING AND TREASURY EFFICIENT ENERGY

EFFICIENT ENERGY SMART TECHNOLOGY

SMART TECHNOLOGY LEGAL ADVISORY

LEGAL ADVISORY WATER MANAGEMENT SOLUTIONS

WATER MANAGEMENT SOLUTIONS

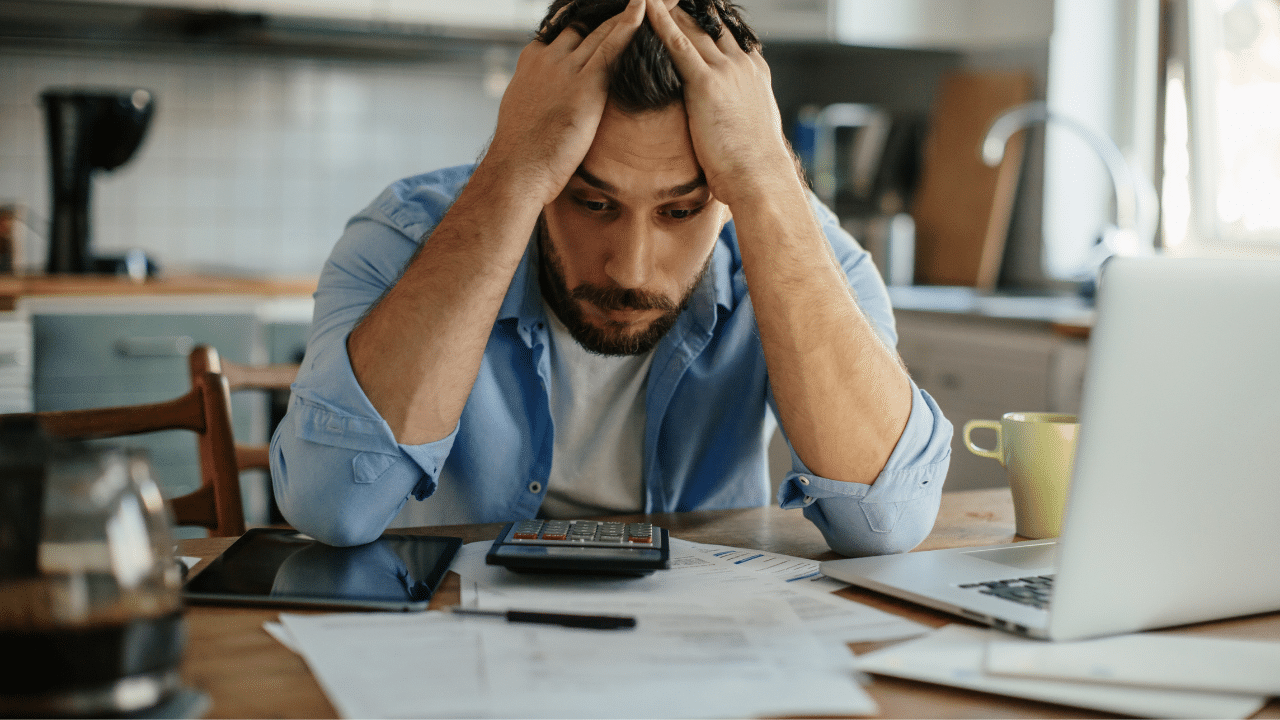

Struggling to pay your levies? Here’s what you can do

Financial hardship can happen to anyone. A sudden job loss, unexpected medical expenses, or broader economic pressures can leave sectional title owners struggling to keep up with levy payments. It’s a situation more common than many realise, and it can have serious consequences not only for the individual owner, but for the body corporate and the entire scheme.

Levies are not optional. They are the backbone of the scheme’s finances, funding everything from basic maintenance and insurance to security and reserve funds for long-term upkeep. When owners stop paying, the body corporate is legally obliged to act. Trustees must take steps to ensure the payment of levies, including the issuing of reminders, handing the matter to attorneys, and, if necessary, taking legal action. This is not punitive; it’s protective. Without consistent levy income, schemes face financial collapse.

So, what can owners do if they genuinely can’t pay? The answer begins with honesty, reflection and decisive action.

Understand the body corporate’s position

Trustees don’t have the discretion to waive levies. Their role is to protect the financial health of the scheme on behalf of all owners. If arrear levies are left unchecked, the body corporate risks falling behind on its own obligations to creditors, contractors and insurers. This could jeopardise everything from insurance cover to municipal services.

Body corporates are encouraged to adopt and implement collection protocols. They ensure fairness, consistency and accountability. But they also mean that ignoring arrears will almost certainly lead to escalating costs.

Communicate early and honestly

The first step is the simplest but most often ignored – tell your trustees or managing agent what’s happening. Silence is seen as unwillingness, while transparency signals good faith. Trustees are more inclined to help if they know you’re engaged.

Reflect on short-term vs long-term hardship

Here is the critical question every owner must ask: Is this a temporary setback, or a permanent change?

- Short-term hardship: If you expect to recover financially in a few months, for example, after medical recovery or securing new employment, a structured repayment plan may be the solution. This allows you to catch up gradually while continuing to contribute to the scheme.

- Long-term hardship: If your circumstances have changed permanently (e.g., ongoing medical care, reduced retirement income, or a job loss without prospects of replacement), repayment plans may only delay the inevitable. Levy arrears accumulate interest and legal costs. Left unchecked, they can consume your equity, leaving you trapped in debt and at risk of losing your home entirely.

This is why self-reflection matters. If you recognise your hardship is long-term, it may be better to take decisive action early. Selling your unit and downsizing to a more affordable home can protect your financial future. It’s a tough decision, but often a far better outcome than letting debt spiral.

Professional guidance from a financial planner can help weigh these options.

Propose a realistic repayment plan

If your issue is short-term, be proactive. Don’t wait for trustees to dictate terms. Present a clear proposal: what you can pay towards your current levies and how much you can contribute monthly towards arrears. Even partial payments show commitment and may prevent legal escalation.

Explore broader funding solutions

Sometimes, arrears stretch beyond one owner. If multiple owners fall behind, the body corporate may face severe cash flow challenges. Contractors, staff salaries, and insurance premiums still need to be paid, and trustees cannot simply delay these obligations.

This is where companies like STS, in partnership with BC Funding Solutions, can play a vital role. By providing access to funding facilities, they allow schemes to remain financially stable while giving owners breathing room to resolve their arrears. It’s a way of balancing compassion for individuals with the collective needs of the community scheme.

Stay engaged and committed

Once you’ve entered into an arrangement, stick to it. Trustees will be far more accommodating if they see consistent effort. If circumstances change, for better or worse, communicate quickly. It is always easier to renegotiate terms than to deal with legal action.

Know your rights and responsibilities

The Sectional Titles Schemes Management Act (STSMA) makes it clear that every owner must pay levies, regardless of personal hardship. Courts have consistently reinforced this. At the same time, owners are entitled to transparent processes and fair treatment. Trustees cannot single anyone out unfairly, but they are required to act when arrears arise.

Conclusion

Falling into levy arrears is stressful, but it doesn’t have to be devastating, provided you act early. The keys are:

- Communicate openly with trustees.

- Reflect honestly on whether your hardship is short-term or long-term.

- Propose realistic repayment plans where possible.

- Take decisive steps, even drastic ones like selling, if your situation won’t improve.

- Explore community-wide funding solutions, like those offered by STS, to protect the scheme as a whole.

The hardest part is often admitting the truth about your financial position. But honesty and early action can protect not just your home, but also the financial stability of your community.

Don’t ignore the problem. Reflect, act, and plan, because doing nothing is the fastest way to lose everything.

MATTHEW KAPP

Legal Professional